Anna Mosna, postdoctoral

researcher at the Leuven Institute of Criminology (LINC), KU Leuven and Giulio Soana, Ph.D. candidate at Luiss

University and KU Leuven

Photo credit: Mario

Taddei, via Wikimedia

Commons

{kind=link}

Introduction

What if we told you

that you can buy a digital image of an ape wearing a crown and heart-shaped

glasses for two and a half million? Well, you may find this a bit pricey. This

does, however, not seem to be a common feeling as images of funny looking apes

have sold, over and over, at stellar prices. This specific project is called

Bored Ape Yacht Club (BAYC) and features 9999 images of apes, each one slightly

different from all the others. The combined value of the collection is

reportedly a dizzying 2.9 billion dollars. This is just one of the many

non-fungible token (NFT) ventures that have been flourishing in the last few

years.

Trade in NFTs represents

a new market that features virtual goods at skyrocketing prices and apparently

little regulation and oversight. With sums of this magnitude at stake, it is

inevitable to think about the repercussions of this new market for illicit

financial flows control. And indeed, NFTs receive increasing attention in the

financial integrity arena. In its ‘2022 Crypto Crime Report’, Chainalysis, one

of the most renowned crypto analytics companies globally, identified a growing

relevance of NFTs to pursue money laundering and wash trading. This risk was confirmed

by the latest virtual assets (VA) report published by the Financial Action Task

Force (FATF) in June 2022. There, NFTs have been recognised as one of the key

market developments to keep under close watch.

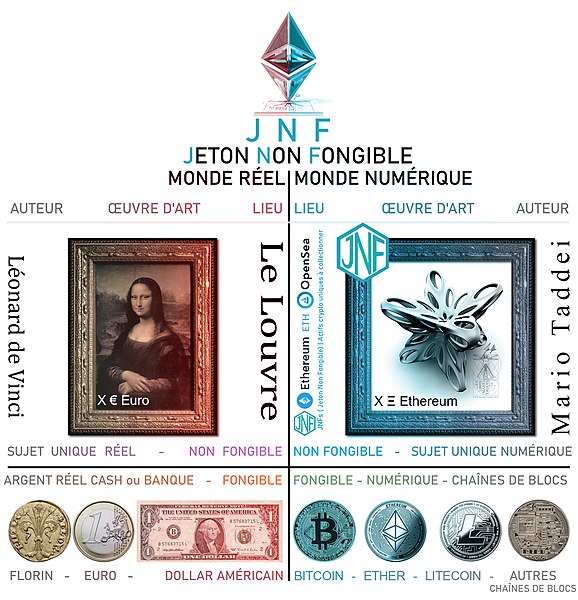

What are NFTs?

Before delving into

the intricacies of the anti-money laundering regulation, a brief introduction on

what NFTs are, is in order. Non-fungible tokens are one of the latest

implementations of blockchain. They exploit blockchains’ immutability and

decentralization to create unique, unalterable, and programmable tokens that can

be freely traded among the participants of the network. On the one hand,

blockchain’s publicity and immutability safeguards the authenticity and

uniqueness of the token while allowing anyone to verify it by, simply,

accessing the ledger. On the other hand, blockchain’s decentralization means

that there is no single entity that can unilaterally modify or control the

status of the token once it is created. The token can both be a digital

representation of a physical or digital asset–as a work of art, a song, or a

ticket to a concert–or solely exist as a digital token. In this latter case,

the value is determined exclusively by the characteristics intrinsic to the

token, its rarity, in case of a token series like BAYC, being an important

factor.

While NFTs may be

used in multiple ways–spanning from the amelioration of the supply chain to the

metaverse–there is one type that presents a particularly high risk in terms of

financial integrity as it is completely decoupled from any pre-existing digital

or physical value: digital art, also referred to as collectible tokens, digital

collectibles or crypto-collectibles. These are, furthermore, the prime and

largest implementation of this technology.

Sharing

characteristics with both virtual currencies and works of art, collectible NFTs

are difficult to frame into a specific category, difficult to regulate and,

thanks to their dynamism, prone to misuse for criminal purposes–including money

laundering. It is therefore interesting to examine where–if anywhere at all–NFTs

can be positioned among the sectors currently covered by the anti-money

laundering (AML) framework applicable in the European Union (EU).

The progressive extension of anti-money laundering rules

– what about NFTs?

Over the years,

anti-money laundering rules have been continuously expanded to address a

growing array of laundering tactics. Control and regulation instruments have

come to cover alongside service providers and intermediaries in traditional

fields, such as the banking sector, also other entities offering financial services,

such as the insurance sector, or operating outside the spectrum of financial

businesses, such as the real estate sector. Increasing awareness of the

potential misuse for the purposes of money laundering and terrorism financing of

virtual currencies, due to the anonymity they ensure, and of art transactions,

nurtured by the speculative nature of prices at which they are carried out, has

triggered a similar extension.

Among others, these

risks have been highlighted, in the FATF Updated 2021 Guidance for a risk-based

approach to virtual assets and virtual asset service providers and, regarding

the art market, already in the FATF 2006 Study on trade-based money laundering.

Likewise, consciousness of these concerns is reflected in the most recent EU legal

instruments in matters of anti-money laundering. The rules enshrined in

Directive (EU) 2015/849 on the prevention of the use of the financial system

for the purposes of money laundering or terrorism financing as amended by Directive

(EU) 2018/843 (Fifth AML Directive) now apply also to entities engaged in

exchange services between virtual currencies and fiat currencies or trading in

works of art.

As obliged entities,

virtual currency service providers and art market actors must carry out customer

due diligence (CDD) that includes know-your client procedures (KYC). As a

result, customers and beneficial owners must be identified and their identity

verified. CDD also requires a continuous assessment of the business

relationship considering its purpose and intended nature. If these compliance

measures cannot be carried out, virtual currency service providers and art

professionals must refuse to carry out the transaction. They further have an

obligation to submit suspicious transaction reports to their national Financial

Intelligence Unit (FIU) and to keep documents acquired in compliance with their

due diligence duties along with supporting evidence and transaction records for

at least five years after the end of the business relationship or after the end

of the occasional transaction. These due diligence duties and record keeping obligations

are intended to ensure more transparency and better traceability of

transactions and to thereby more effectively prevent and, possibly, enforce

laundering activities occurring in the trade with virtual currencies and in the

art market.

The considerations

that led to the inclusion of these two sectors within the scope of application

of AML rules suggest that there is a comparable need to do the same with the

trade in NFTs. NFTs are similar in nature to virtual assets and, at times, to

works of art. These tokens even combine and magnify the respective risk factor

of each of these two categories. Like virtual assets, NFTs are immaterial and

can be exchanged globally and instantaneously in a pseudonymous fashion. Like

works of art and collectibles, NFTs have a variable and subjective price that

can be artificially inflated.

Against this

background, the question about the extent to which existing AML rules are

already applicable to the trade in NFTs imposes itself. The answer, which is

likely to differ according to the use made of the NFTs considered, will depend

on the possibility to actually subsume NFTs under the concept of goods whose

trade is already regulated. In short: virtual assets, virtual currencies or

works of art.

Non-fungible tokens as virtual assets and virtual

currencies

The link between NFTs

and virtual assets is an obvious one. With virtual assets, NFTs share the

technology they both predominantly employ, the blockchain. Most NFT projects

are even rooted in an infrastructure–Ethereum–that issues a coin–the Ether–that

is classified as a VA. It is, then, natural to wonder if these tokens are

themselves virtual assets and, thus, if they fall within the scope of the same

financial integrity regulation as VAs.

Virtual assets have

been, since 2014, object of a progressively stringent regulation. Through ad-hoc

guidelines, the FATF has extended to numerous players in the VA world–such as

exchangers, wallet providers–registration and compliance duties. According to

the FATF glossary, virtual assets are ‘a digital representation of value that

can be digitally traded, or transferred, and can be used for payment or

investment purposes’. Notwithstanding the distinct similarity to such assets, according

to the FATF, NFTs are, in principle, not considered to be virtual assets. As

provided by the above-mentioned 2021 Guidance, ‘[d]igital

assets that are unique, rather than interchangeable, and that are in practice

used as collectibles rather than as payment or investment instruments […] depending

on their characteristics, are generally not considered to be VAs under the FATF

definition’.

This exclusion does

however not imply that NFTs are entirely exempt from the application of

anti-money laundering rules. As the FATF Guidance clarifies, this definition of

‘virtual assets’ must be interpreted broadly and functionally–meaning: through

the analysis of the concrete function of the analysed asset. First, the FATF specifies

that the exclusion only covers tokens that are used as collectibles. If NFTs

are used in practice as means of payment or investment, they would still fall

within the definition of VA and, one could add, also within that of ‘virtual

currencies’ as coined by the Fifth AML Directive. The Directive defines virtual

currencies as ‘a digital representation of value that is not issued or

guaranteed by a central bank or a public authority, is not necessarily attached

to a legally established currency and does not possess a legal status of

currency or money, but is accepted by natural or legal persons as a means of

exchange and which can be transferred, stored and traded electronically’.

Second, the

exclusion of NFTs from the scope of the VA regulation does not preclude collectible

NFTs from falling, depending on their concrete use, within a different category

of regulated asset. This would, for instance, be the case where NFTs are

digital representations of other financial assets that are already covered by

FATF standards. Also in this case, the AML regime governed by the Fifth AML

Directive may apply.

Non-fungible tokens as works of art?

What if NFTs are

not used as means of payment or investment, but indeed only used as

collectibles? Parallels between NFTs and works of art are, unlike those between

NFTs and VAs, not structural but content-related. Collectible NFTs encapsule (digital)

art. Can they therefore be defined as ‘works of art’ within the meaning of the

Fifth AML Directive?

The Fifth AML

Directive does not provide for a definition of the concept of ‘works of art’.

Even without considering digital contents, this raises the question as to

whether only those who trade in so-called ‘fine art’ are subject to the EU AML

regime or whether these rules apply also to those who trade, more generally, in

cultural objects including, hence, antiquities. As was foreseeable, national

implementation laws reflecting different sensitivities towards the need to

protect cultural heritage have based their provisions upon different

understandings of what ought to be considered a work of art.

Member States with

considerable wealth of antiquities and a long-standing tradition of strict

cultural heritage protection laws, such as Greece or Italy, have adopted a broad

notion of works of art and extended national anti-money laundering rules to

those trading in fine art and to those trading in antiquities. States that are

mainly market countries for cultural objects, such as Germany and the United

Kingdom–where the Fifth AML Directive was implemented before Brexit–have opted

for a narrower concept of ‘works of art’. Aligning their definition to the one

provided in their respective laws on value added tax, they apply their AML

regime to those who trade in paintings, drawings, engravings, sculptures and

other objects that can be entirely executed by hand. The trade in antiquities

is included insofar as the antiquities traded qualify as paintings, drawings,

engravings, sculptures. This understanding excludes antique furniture, coins

and stamps collections from the concept in question.

A workable

definition of ‘works of art’ based on the lowest common denominator that has

informed national implementations comprises objects that are individually conceived

and executed by a person by hand or, one could reasonably add, with the help of

different techniques and technologies, as long as the creative process remains human-initiated.

Revolving around the two focal points of human creativity and uniqueness this definition

excludes objects that are the result of automated reproduction of a potentially

unlimited series of identical items. The question now is whether, applying this

criterion to digital art, it would allow to identify collectible NFTs, such as

those containing an image of an algorithm-generated Bored Ape, as a work of art

as envisaged by the Fifth AML Directive.

The societal

perception of NFTs such as the Board Apes is already that of iconic images, of

art. This is confirmed by the fact that collectible NFTs are sold in digital

galleries and at digital auctions–as was the case with the NFT ‘Everyday: The

First 5000 Days’ by Mike Winkelmann, known as Beeple, that was sold for 69.3

million dollars with fees at Christie’s in early 2021–and, most importantly, by

the fact that many artists that have been creative outside the Web3.0–Marina

Abramović being an eminent example–consider this kind of NFTs as a new,

attractive form of artistic outlet.

From a legal

standpoint, the concept of ‘work of art’ included in the Fifth AML Directive seems

equally to allow for such an inclusion: NFTs are by definition unique and those

who are relevant as collectibles–let’s think about the Bored Ape collection, about

Beeple’s ‘Everyday: The First 5000 Days’ or about Marina Abramović’s ‘Hero

25FPS’–are the result of human ingenuity and creativity. That being said, as

the concrete application of the AML regime designed by the Directive in

question depends on national legal instruments implementing its provisions and

given that many national laws, like the relevant German framework, identify

works of art through lists of categories of objects, it is likely that

legislative adjustments may be necessary at that level before the current AML rules

are capable to govern the trade in collectible NFTs as well.

Concluding remarks

The general

exclusion of collectible NFTs from the purview of the VA regulation does not

equal an automatic exclusion of the trade in NFTs from the scope of application

of AML rules. Depending on the concrete use that is made of NFTs, they may

still be considered virtual currencies or fall within the scope of a different

category of regulated assets. This is particularly meaningful in regions, like

the EU, where a more stringent regulation than the one envisaged by the FATF

has been adopted: it suffices to think of the application of the travel rule to

unhosted wallets.

Furthermore, the EU

AML regime extends also to the trade in works of art–a category, as has been argued above, under

which collectible NFTs could be subsumed. Collectible NFTs appear, indeed, to

fulfil the basic requirements of ‘works of art’ as identified by laws

implementing the Fifth AML Directive. An extension of the AML regime is

therefore possible and, perhaps, not entirely inappropriate in light of the very

nature of collectible NFTs: as digital art, they are susceptible to highly

subjective, at times arbitrary price-setting. This feature is exacerbated when

NFTs exist only as digital tokens. In that case, they do not have any relation

to a pre-existing digital nor to a physical artistic expression that could act

as a possible parameter for such pricing.

Wherever prices can

be modified at will and single transactions exceed several millions of dollars–or

euros, or pounds–there is an inherent and, arguably, quite sensitive risk of

money laundering. Introducing regulation and control appears therefore to be a

sensible consideration. As a matter of fact, the policy discourse surrounding

NFTs of the last year shows how both the private and the public sector are

eager to discuss such measures for the trade in NFTs. This also shines through

the Proposal for a Regulation on markets in crypto-assets (MiCA) that is

currently undergoing the ordinary legislative procedure. While it does not seem

that NFTs will be included in the definition of ‘utility token’ nor, in

principle, in the scope of application of MiCA–in line with their positioning

regarding FATF standards–Recital 8b that has been newly added to the Proposal

for the Regulation refers to the need to reflect on a separate legislative

proposal of an EU-wide regulatory regime for NFTs.

This comment has been removed by a blog administrator.

ReplyDeleteThis comment has been removed by a blog administrator.

ReplyDeleteThis comment has been removed by a blog administrator.

ReplyDeleteThis comment has been removed by a blog administrator.

ReplyDelete